Just Three Words — Endless Applications

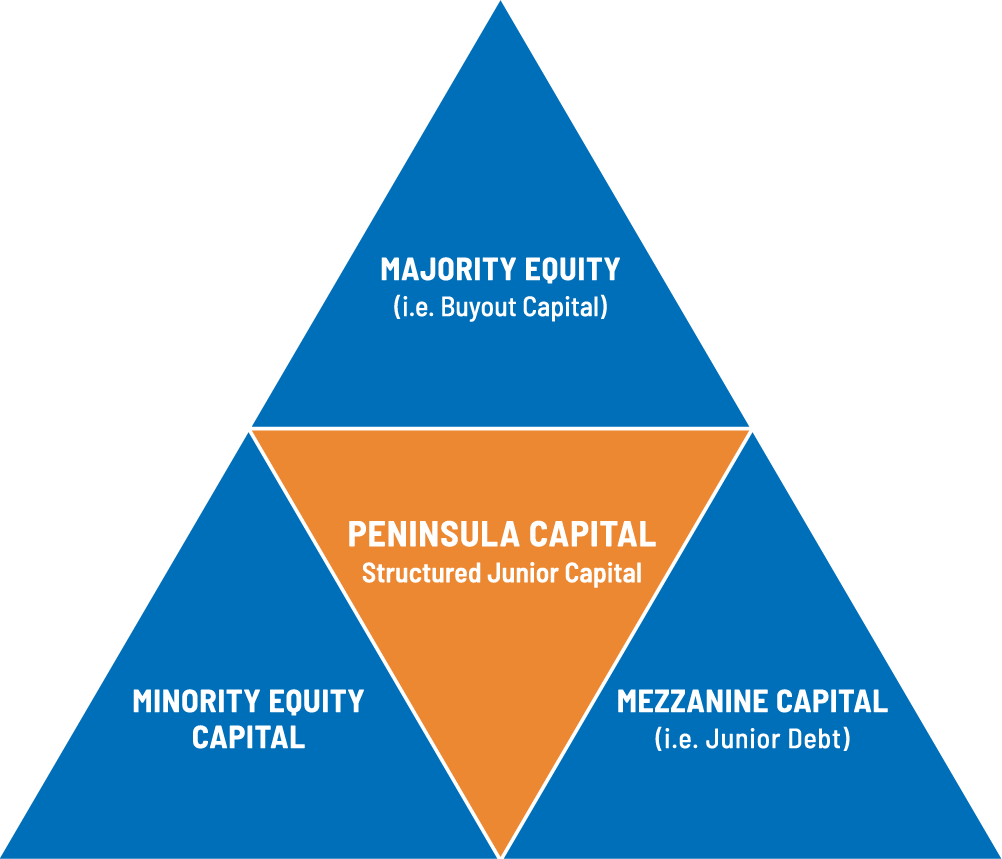

What is Structured Junior Capital?

Structured Junior Capital is a catch-all term for equity and/or junior debt tranches structured specifically to address the funding requirements of a leveraged transaction.

What Types of Transactions Require It?

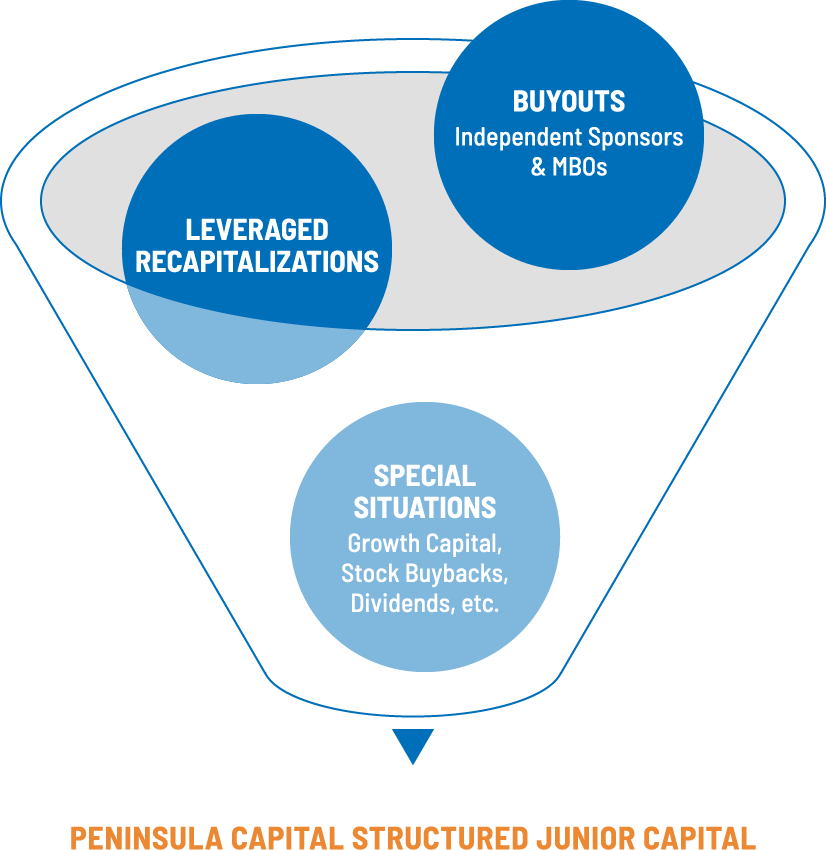

Buyouts and recapitalizations are the most common leveraged transactions that require one or more tranches of structured junior capital, but any transaction requiring more funding than is prudently available via senior borrowings is a candidate.

How are Investments Structured?

Based on the amount of capital being sought, the type of business, the availability of senior debt, preferences of other investors and expected future funding needs of the business, a junior capital solution is tailored to meet the specific transaction and business requirements. For most Peninsula Capital transactions, this takes the form of both an equity and junior debt (i.e., mezzanine or subordinated debt) tranche.

How is this Different Than Traditional Mezzanine or Buyout Capital?

In short, it’s broader in transactional scope and application. Most mezzanine capital investors are mostly (or entirely) subordinated debt lenders, and are often strictly minority equity investors. Buyout funds are nearly always majority equity investors, and typically not able, or willing, to also provide junior debt tranches. By contrast, structured junior capital includes all transactional funding needs, customized to the specific transaction’s requirements and participants’ preferences.

Why Peninsula Capital Partners Structured Junior Capital?

Peninsula Capital is one of the very few middle-market capital providers that supports the full spectrum of structured junior capital transactions, including minority or majority equity positions, participant or sponsor roles, and debt and equity capabilities as required by the transaction and participants’ goals and objectives.

Peninsula is a fantastic partner; a firm that leverages their extensive experience to approach problems and opportunities creatively.”

Read MoreSteven P. McGrath

Managing Partner, Level Capital Partners, LLC

We are now better positioned than ever to serve our clients with a level of global talent and expertise that is setting a new standard for agency partners. Thank you to Karl LaPeer, Andrew Wiegand, Dennis Murphy and the team at Peninsula for supporting us at every turn the last 7+ years.”

Read MoreKatie Briscoe

CEO, MMGY Global

From the very beginning, we have had a very collaborative and enjoyable partnership with Peninsula. We built camaraderie through challenges that could stress relationships. ”

Read MoreJohn Harrison

Managing Partner, A111 Capital

It has been a pleasure to work with the people at Peninsula. During good times, they have been supportive of our growth. When our business faced challenging economic times, their trust in our management team, financial support and willingness to adjust our capital structure helped to navigate to a stable and healthy position.”

Read MoreRandy Gottlieb

CEO, Hygrade

To find a partner that shared our passion was a prerequisite that we thought we’d struggle to find, but from the get go Peninsula showed a real understanding and empathy for our business and the people within it. We’re over a year in and we’re delighted with our decision and remain firmly on track to achieve our ambitious long-term goals.”

Read MoreSimon Davison

Founder, Escapology

Partnering with Peninsula has been one of the best decisions we have made thus far as an independent sponsor. The team is highly disciplined, applies strong analytics and consistently displays a high level of integrity….”

Read MoreEdwin Burke

Managing Partner, Pillsman Partners, LLC

When we sold our company to Peninsula, I had many questions, and some anxiety, about how we would be treated post-deal. Seven years later, all of those questions have been answered. It could not be a more fulfilling (and successful) partnership.”

Read MoreClayton Reid

Executive Chairman, MMGY Global, LLC

Over the past seven years, Peninsula Capital Partners has been instrumental in supporting the Burlington Team’s transition from a small unsophisticated company to a global leader in the radiation protection industry.…”

Read MoreLee Ann Fachko

CEO, Burlington Medical, LLC

In my experience, strategic alignment of stakeholders is the most critical element of success for a private equity-backed business. The Peninsula team does a fantastic job of communicating with management to ensure such alignment.…”

Read MoreBurton Heiss

CEO, Escapology

…Our client had an instant connection with the Peninsula team, which carried all the way through negotiations, due diligence and the inevitable complexities that emerge in any transaction.…”

Read MoreChris Goeglein

Managing Principal, True North Strategic Advisors LLC

… James Illikman and Peninsula took a different approach and looked at the longer-term opportunity and invested the time and resources into making the business stronger.”

Read MoreClark McKeown

President & CEO, Wild Wing Hospitality Inc.

Chris Gessner and Peninsula have been our go-to capital partner for years now. Their ability and desire to work through difficult and challenging deal issues sets them apart from other capital partners.

Read MoreGreg Bregstone

Partner, Woodlawn Partners

I strongly recommend that you consider Peninsula Capital as your business partner.

Read MoreDavid Janks

President, Power Vac, LLC

We Span the Whole Capital Structure

Peninsula Capital’s Structured Junior Capital investment approach allows for customized funding solutions that span junior debt to majority equity positions, and everything in between. Our rare flexibility allows us fill a variety of capital structure roles, from being solely a subordinated debt investor, to a one-stop capital provider that funds all the equity and junior debt required to complete a transaction. We are equally capable of participating in a deal led by an independent sponsor or leading a transaction in a sponsorship role, depending upon what the situation requires.

We Cover the Full Range of Middle-Market Transactions

Peninsula Capital’s Structured Junior Capital investment approach is not limited to simply change-of-control transactions, but rather is applicable to any leveraged transaction requiring junior capital. From Independent Sponsor-led buyouts to leveraged recapitalizations to growth capital rounds, we can formulate an unique funding solution that is responsive the needs, objectives and preferences of the transaction and its participants.

Peninsula is a fantastic partner; a firm that leverages their extensive experience to approach problems and opportunities creatively.”

Read MoreSteven P. McGrath

Managing Partner, Level Capital Partners, LLC

…Our client had an instant connection with the Peninsula team, which carried all the way through negotiations, due diligence and the inevitable complexities that emerge in any transaction.…”

Read MoreChris Goeglein

Managing Principal, True North Strategic Advisors LLC

Partnering with Peninsula has been one of the best decisions we have made thus far as an independent sponsor. The team is highly disciplined, applies strong analytics and consistently displays a high level of integrity….”

Read MoreEdwin Burke

Managing Partner, Pillsman Partners, LLC

Chris Gessner and Peninsula have been our go-to capital partner for years now. Their ability and desire to work through difficult and challenging deal issues sets them apart from other capital partners.

Read MoreGreg Bregstone

Partner, Woodlawn Partners

I strongly recommend that you consider Peninsula Capital as your business partner.

Read MoreDavid Janks

President, Power Vac, LLC

To find a partner that shared our passion was a prerequisite that we thought we’d struggle to find, but from the get go Peninsula showed a real understanding and empathy for our business and the people within it. We’re over a year in and we’re delighted with our decision and remain firmly on track to achieve our ambitious long-term goals.”

Read MoreSimon Davison

Founder, Escapology

We are now better positioned than ever to serve our clients with a level of global talent and expertise that is setting a new standard for agency partners. Thank you to Karl LaPeer, Andrew Wiegand, Dennis Murphy and the team at Peninsula for supporting us at every turn the last 7+ years.”

Read MoreKatie Briscoe

CEO, MMGY Global

… James Illikman and Peninsula took a different approach and looked at the longer-term opportunity and invested the time and resources into making the business stronger.”

Read MoreClark McKeown

President & CEO, Wild Wing Hospitality Inc.

When we sold our company to Peninsula, I had many questions, and some anxiety, about how we would be treated post-deal. Seven years later, all of those questions have been answered. It could not be a more fulfilling (and successful) partnership.”

Read MoreClayton Reid

Executive Chairman, MMGY Global, LLC

From the very beginning, we have had a very collaborative and enjoyable partnership with Peninsula. We built camaraderie through challenges that could stress relationships. ”

Read MoreJohn Harrison

Managing Partner, A111 Capital

In my experience, strategic alignment of stakeholders is the most critical element of success for a private equity-backed business. The Peninsula team does a fantastic job of communicating with management to ensure such alignment.…”

Read MoreBurton Heiss

CEO, Escapology

It has been a pleasure to work with the people at Peninsula. During good times, they have been supportive of our growth. When our business faced challenging economic times, their trust in our management team, financial support and willingness to adjust our capital structure helped to navigate to a stable and healthy position.”

Read MoreRandy Gottlieb

CEO, Hygrade

Over the past seven years, Peninsula Capital Partners has been instrumental in supporting the Burlington Team’s transition from a small unsophisticated company to a global leader in the radiation protection industry.…”

Read More